2026 Federal Budget

Implications for Capital, Structure & Long-Term Decision Making

Core Themes

- Erosion of policy credibility → retrospective-style changes, reliance on grandfathering

- Capital disincentivised → higher friction on risk-taking and long-duration assets

- Shift toward income over growth → structural bias to yield over capital appreciation

- Consumption over accumulation → reduced incentives to defer, save, and invest

- Redistributive tilt → intergenerational and class-based policy framing

- Expansionary fiscal stance → structurally inflationary bias

- Grandfathering critical → outcomes depend heavily on timing and asset base

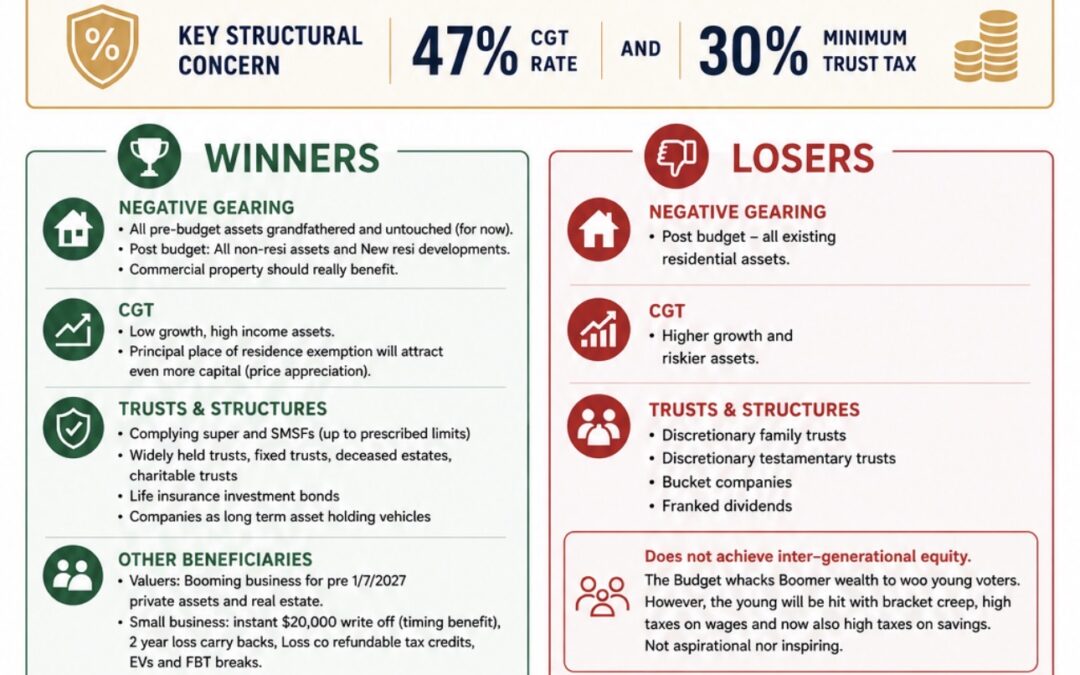

Key Structural Concern

- 30% minimum tax on trusts

- 47% top tax rate on capital gains, with a 30% minimum tax rate

- Double taxation risk → corporate profits taxed at company level + constrained extraction pathways

Winners

Negative Gearing

- Pre-budget assets fully grandfathered

- Post-budget: new residential + all non-residential assets remain eligible

- Commercial property → likely relative beneficiary

CGT Regime

- Favours low-growth / high-yield assets

- Principal Place of Residence (PPOR) → increased capital allocation → upward price pressure

Structures

- Complying super / SMSFs (within caps)

- Widely held & fixed trusts

- Deceased estates & charities

- Life insurance / investment bonds

- Companies as long-term holding vehicles

Secondary Beneficiaries

- Valuers → demand surge pre–1 July 2027 (cost base resets)

- Small business

- $20k instant asset write-off (timing benefit)

- 2-year loss carry-back

- refundable loss credits

- EV / FBT concessions

Losers

Negative Gearing

- Post-budget existing residential property → materially less attractive

Capital Gains

- Higher-growth / higher-risk assets → penalised

Trust Structures

- Discretionary family trusts

- Testamentary discretionary trusts

- Bucket company strategies

- Franked dividend streaming

Intergenerational Reality

- Policy framed as targeting “established wealth”

- In practice:

- Younger cohorts face bracket creep + wage taxation

- Now also higher tax on savings and investment returns

Outcome:

→ Weakens aspiration, capital formation, and long-term ownership culture

Action Points

- Valuations before 1 July 2027 → reset CGT cost bases

- Revisit trust distributions → shift toward fees, salaries, retained structures

- Structure review → migration toward companies, bonds, compliant vehicles

- Asset decisions → assess crystallisation vs deferral of embedded gains

- Advocacy → engage on policy credibility and investment incentives

What Comes Next?

- Extension of tax base toward:

- Principal residence (PPOR)?

- Inheritance / death taxes?

Closing Observation

This Budget marks a structural shift in how capital is treated in Australia:

From encouraging accumulation and risk-taking

→ toward managing distribution and stability

The long-term consequence will depend not on the headline rates,

but on how capital adapts through structure and behaviour.

Should you wish to discuss these matters, and how they may impact you, please do not hesitate to contact us.

#Budget #CGT #Trusts #NegativeGearing #CapitalAllocation #Structuring #PolicyRisk